You’ve just wrapped up a project for your overseas client. They say, “Payment sent via bank transfer — should hit soon.”

You nod, smile politely, and wait.

Two days later, your bank credits you ₹81,500 for what was supposed to be $1000. You check again. You refresh. You sigh.

Where did the rest go?

That, right there, is the *Bank SWIFT experience* in a nutshell — layers of invisible fees, mystery FX rates, and three middlemen who each take a tiny bite before the money finally lands in India.In contrast, **Wise** promises speed, transparency, and a simple answer to that universal freelancer question: *“How much do I actually get?”*

So let’s strip away the guesswork and see, once and for all, which one helps you bring home a better landed INR.

Why This Comparison Matters

For Indian freelancers and small exporters, USD inflows are life blood. Every rupee shaved off by hidden spreads or delays eats into your profit margin.

Bank SWIFT has been around for decades — and it works. But it’s slow, complex, and opaque. You’re lucky if you even find out what exchange rate your bank used.

Wise, on the other hand, uses local banking networks, converts at mid-market FX, and shows you every fee before you hit “send.”

The difference? “Predictability. Transparency. Speed.”

And sometimes, that difference equals a few hundred rupees you didn’t know you were losing.

How SWIFT Transfers Work (And Why They Cost More)

SWIFT isn’t a payment system. It’s a **messaging network** — a secure way for banks to talk to each other.

Your money doesn’t travel directly from your client’s account to yours; it hops through two, sometimes four, intermediary banks before reaching India.

Each hop can trigger deductions or currency conversions that no one tells you about in advance.

| Step | Description | Fee Impact | Time |

|---|---|---|---|

| Sender’s Bank | Initiates SWIFT wire | Outward fee (~$15–$30) | 0–1 day |

| Intermediary Banks | Route payment | Deducts handling fees | +1–2 days |

| Recipient Bank (India) | Converts USD→INR | Applies FX margin (1.5–3%) | +1–2 days |

So even though your client sent $1000, you might receive $950 or less. And if you ever try to track where it went? You’ll be met with a shrug and an email chain.

How Wise Transfers Work (And Why They Often Win)

Wise flips that model on its head.Instead of sending money through global banking pipes, it uses “local accounts” on both sides.When your client sends USD to Wise, it doesn’t physically cross borders. Wise already holds USD and INR locally — it just matches and settles internally, using the **mid-market rate** you see on Google.

Here’s what that looks like in practice:

| Step | Description | Fee Impact | Time |

|---|---|---|---|

| Client pays via Wise | USD debit or card | ~0.5–0.8% fee | Instant |

| Wise converts USD→INR | Mid-market rate + minimal markup | Transparent | 1–2 days |

| INR credited to Indian account | Auto FIRC issued | None | 1–2 days |

No intermediaries. No “missing” dollars. No waiting five days for your bank to locate a remittance sitting in Frankfurt.

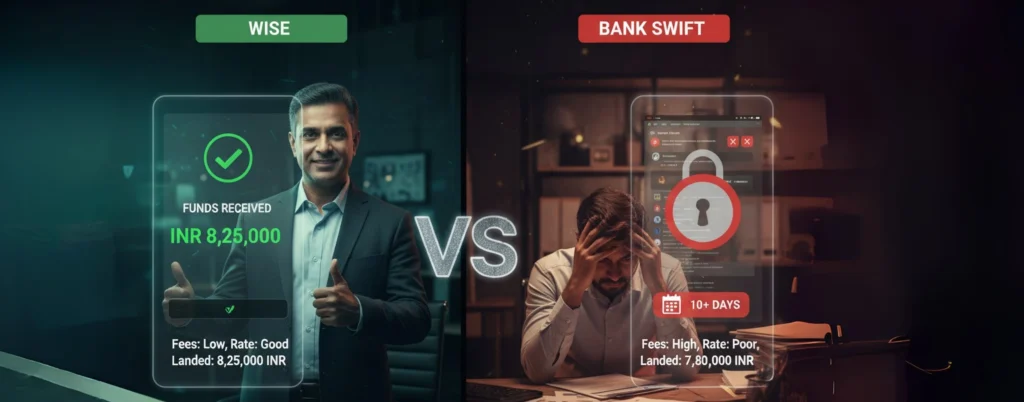

Real Example: $1000 USD Payment

| Platform | USD Sent | Total Fees | FX Rate | INR Credited | Time Taken | FIRC Process |

|---|---|---|---|---|---|---|

| Wise | $1000 | $7 | ₹83.10 | ₹82,430 | 1–2 days | Auto-generated |

| Bank SWIFT | $1000 | $30 (avg) + $20 intermediary | ₹82.00 | ₹81,500 | 3–5 days | Manual via bank |

At first glance, you might think, “₹900 doesn’t matter.”But if you’re a freelancer billing $4000 a month, that’s ₹3,600 gone — every single month — just for choosing the wrong pipe.Over a year? That’s ₹43,000. Enough for a laptop upgrade, your next software stack, or three months of rent.

Compliance and FIRC Handling

Both Wise and Bank SWIFT are fully RBI-compliant. But the way they handle **documentation** is night and day.

SWIFT:- Your FIRC (Foreign Inward Remittance Certificate) is issued by your receiving bank. It can take days, even weeks, and often needs a manual request.

Wise:- Works through Indian partner banks like Yes Bank and HDFC, issuing an **e-FIRC automatically** with every payment.

For anyone dealing with tax filings or GST refunds, this automation isn’t a nice-to-have — it’s a sanity-saver.

Security and Trust

Let’s be clear: both systems are safe.

SWIFT:- A global network used by over 11,000 banks for 50 years.

Wise:- Licensed in India, regulated by the FCA (UK) and other financial authorities worldwide.

The real difference isn’t about *safety* — it’s about **visibility**.

Wise tells you what’s happening at every step. SWIFT keeps it behind glass.

Summary Table — Wise vs Bank SWIFT

| Feature | Wise | Bank SWIFT |

|---|---|---|

| Fees | ~0.7% | $25–50 fixed + FX markup |

| FX Transparency | High (Google rate) | Low (hidden markup) |

| Speed | 1–2 days | 3–5 days |

| Intermediaries | None | 2–4 banks |

| FIRC | Automatic (e-FIRC) | Manual (bank issued) |

| RBI Compliance | Yes | Yes |

| Best For | Freelancers, SMEs | Large corporate transfers |

Verdict — Who Wins the Landed INR Race

For freelancers and service exporters, **Wise almost always wins** the landed INR race.

It’s faster, cheaper, and clearer.For large-value B2B transactions (say above USD 50,000), traditional SWIFT channels can still make sense — especially if trade credits, LCs, or intermediary compliance layers are involved.But for most small exporters and freelancers, the equation is simple:

Transparency beats tradition

You shouldn’t need a magnifying glass to know where your money went.

Freelancer Checklist Before Choosing

* Compare landed INR for each option (not just the exchange rate).

* Clarify who bears the intermediary fees.

* Confirm how and when your FIRC is generated.

* Keep every payment receipt — especially for SWIFT remittances.

* Track your settlement times — consistency matters as much as cost.

In Summary

Both Wise and Bank SWIFT get your dollars to India — but one moves at fintech speed, while the other still runs on 1980s rails.

Wise shows you what you’ll get upfront; SWIFT makes you find out later.And for independent professionals, that difference means more control, fewer surprises, and better planning.But here’s the thing — if you want the transparency of Wise and the dependability of a fully compliant banking backbone, you don’t have to choose between the two anymore.

HiWiPay is built precisely for Indian exporters, freelancers, and businesses that live on global income. It offers fast, RBI-compliant cross-border payments, zero hidden markups, automatic e-FIRC and e-BRC generation, and 24-hour INR settlement — all in one intuitive platform that finally makes receiving overseas money feel effortless.

If you’ve ever thought, “I just want my dollars to land right — without the drama,”

HiWiPay was built for that exact moment.

Up next: HiWiPay vs Wise — Finding Your Real Landed INR

(Because what matters isn’t what’s sent — it’s what finally lands.)